THE SPELL-CASTERS

Back in the stone age, when I was a teenager, I had the good fortune of hanging out with a pretty eclectic group of people. Among this group were a certain subset who might be called spell- casters. These were individuals who, quite literally, cast spells to deal with the problems of everyday life: to get the girl, the promotion, or even just pay the bills. Hanging out with this crew didn’t score many points with the authorities at the conservative Catholic school I attended. Some, no doubt well meaning, busybody actually informed my parents that my soul was in danger. Had this person , or the school priests, who wished to save my soul, actually been able to step inside my mind, they wouldn’t have sought to sever my ties to the “devil worshipers”; they would have confiscated my copies of Carl Sagan’s Dragons of Eden and Cosmos, they would have burned my worn out paperback of Nietzsche’s Beyond Good and Evil, and forced me to read the Christian heavy hitters of Kierkegaard and Dostoevsky, the latter who I especially adored.

I was not a member of the spell- casters, I was more like their sceptic mascot. I really enjoyed sparring with them, and it may seem odd, but I think they felt the same. For both me, and for them our arguments were ways to clarify our own thinking, to chart our divergent spiritual paths. I don’t remember much of anything but the tenor of these discussions except for one, and it has stuck with me all of these years.

Once, I was asking one of the spell- casters to explain to me the physical mechanism for how they were supposedly able to influence others with their ritual mumbo-jumbo. Was it brain waves? Pheromones? What?

Without really hesitating he responded that“it was like money”.

What?!

He continued that “money was a talisman, that grants its holder power because others believe in its power” that he, as a spell-caster, really only had power over those who already believed he had power to begin with, that I, as a sceptic, was largely untouchable, in a way that those, such as the Church who believed in his magic, but just thought it came from a place of darkness, were not.

The idea stuck in my head… money was a talisman.

Years later I encountered this same idea in a totally different context in William Greider’s conspiratorial sounding: Secrets of the Temple, How the Federal Reserve Runs the Country. I have not been able to locate my old, no doubt, dust covered copy of Greider’s excellent book, and have not read it for perhaps a decade, but I will try to remember as best as I can, and will turn to Greider when I come to the issue of the Federal Reserve.

As far as money being a talisman, Greider, from what can I recall, repeated the same point as my spellcaster friend. Money had something of our primitive magical thinking behind it, we had to believe in it to make it real.

I came back to this idea in the context of this series of posts because it seemed to suggest something about the connection between our current economy and idolatry. I thought for sure I would be able to find all sorts of evidence for money having originated as a talisman- which, by the way, is different than what we would call a charm- say your lucky rabbit’s foot. A talisman is an amulet that covers certain powers, such as powers of seduction, or the power to attract wealth etc.

I was able to find anecdotal evidence that money came into the world as a talisman. Take the picture above. On the left is a picture of traditional Chinese coin (Tang Dynasty 7th and 8th centuries AD), and on the right is a traditional Chinese talisman. (Shang Dynasty 16th- 11th centuries BC). I, for one can’t tell the difference, but such does not an argument make.

Instead of finding surefire evidence that money had originated as a talisman, in my search, I discovered a fascinating story about the origins of money and debt themselves: David Graeber’s Debt the First 5,000 years, and it is from there that I think this inquiry should continue.

Graeber sets out to tell the history of debt, but this seems to require that he provide a history of money, for the two are inseparably combined. Like many other people, I had always imagined that money had emerged as an advance over systems of barter.

But, as long as we take the findings of economic anthropologists and economic historians into account, this idea appears to be a myth. According to Graeber not one anthropological or historical example of money emerging spontaneously from barter has been observed.

Historically, money seems to have first appeared in Ancient Sumer as a form of temple credit, allowing priests to keep accounts with the local population, and then evolved into a more general system of credit-money. Niall Ferguson, in his documentary, The Ascent of Money, has a cool scene (@9 min) in which he is holding one of these clay credit-money pieces in his hand. It’s inscription reads that the possessor of the tablet is owed so much grain by such-and-such. That “possessor” part is important because it implies that these tablets were transferable.

In Graeber’s tale, this credit money was supplanted by coinage with the rise of empires. He sees the dual-evolution of coinage and the state this way: the state needed to pay its new professional soldiers in some way, and money was an ingenious way they could do so. The state created coins, gave them to its soldiers, and then asked for them “back”, not from the soldiers, but as a tax on its merchants and farmers. These merchants and farmers were thus compelled to accept payment for their goods from soldiers in the the form of the state’s coins. The state had created its own perpetual motion machine- for war.

Many people on the right today, at least in America, seem to associate “hard-money”, that is money backed by gold, with a weak state. Graeber thinks the relationship actually worked the other way around. Hard- money is the surest sign of a strong state, and the vector through which the state imposes taxes. Eras of hard-money are also incredibly violent, after all, they signal that large armies are marching around. They tend as well to be eras of mass slavery- classical, African. The two major hard-money eras, in the West, Graeber thinks, were those between the birth and fall of the Roman Empire, and the period from the early 1400s to the mid-20th century.

Hard-money has a rival in the form of credit-money, and the two tend to oscillate over great arcs of history and over a very wide historical expanse. The great period of credit-money was from the fall of the Roman Empire until the early 1400s, and its most important developments took place outside of the West. Both China, and the Islamic World, had thriving, credit-based economies for much of this era. The Islamic World, especially, developed a rich market-based economy that was largely free from government interference, and many of the financial innovations that later made their way to Europe were begun here.

Periods of credit-money have a tendency to also become eras of debt, and this debt can sometimes be horribly de-humanizing. As the father of two daughters, the idea of the “bride-price” struck me on a particularly visceral level. In certain eras and places daughters became “collateral” for loans. This was actually the standard by which the dark age Irish judged something’s worth, by the abstract value of not just another human being, but your very own child.

The answer that credit-based societies have come up with for the problem of debt is essentially to ban interest on loans, especially high rates of interest, or usury. Graeber sees no anti-commerce logic to these bans on charging interest. Muslim society, for instance, has been, and is, an extremely commerce based society that, even to this day, largely looks askance at interest bearing loans.

The Catholic Church, having taken Aristotle seriously, held that interests bearing loans had something unnatural about them. Money, in ages where it is based on credit and not coin, was seen as a social convention, nothing more, and nothing less. Charging interest on a “mere idea” seemed to the Medievals to be asking something lifeless to generate itself, to have “money beget money” in the same way life begat life.

The credit-money era of the Middle Ages did not so much end as became a hybrid-era of both credit-money and cold hard cash, and it was this hybrid quality which I think Graeber is suggesting helped give rise to capitalism, which really was something new under the sun.

A barbarian like Hernando Cortez was literally insatiable for the gold of the Americas, and it’s this insatiable quality which was somewhat new. Why did Cortez not rest free and easy on a caribbean island after he had won the lion’s share of the biggest of the biggest gold booty in history- the riches of Tenochtitlan? Graeber suggest it was because he was in debt up to his eyeballs with interest bearing loans he could never hope to repay- even though he had conquered one of the greatest empires on the globe.

It was this idea of being designed for limitless growth that was new, something that came into being most clearly a half a century after the death of Cortez with the creation of the Dutch East India Company. This company was a public-private partnership whose mission was the domination of the spice trade, which paid its soldiers in gold coins, and was built from loans- in the form of shares- that could never be repaid but required the outlay of “dividends” to the stockholders. Issuing more stock for supplies for imperial expeditions, meant more dividends would have to be paid, and therefore the gain of more control over the spice trade secured- a control that was largely “bought” by the force of arms.

Here I am going to step aside from Graeber, and lean on what I can remember from William Greider’s Secrets of the Temple, for while Graeber is great on economic history up until the slave trade, his take on contemporary history is a little thin and I think Greider can fill in that gap.

Since the 1700s, we seem to have been slowly moving back towards the idea that money is a social convention. Since then we have oscillated between hard-money (paper backed by gold) and soft-money (paper based on credit) with every era of hard-money seeming to end in a deflationary crisis as money dries up, goods plummet in value, and loans become unbearable, followed by an era of soft- money, in which credit chases its’ own tail, goods become too expensive to buy, and manic asset bubbles emerge, some large enough to take down whole economies.

The problem is simple to state, and incredibly hard to solve. If money is a convention then we can make as little of it or as much of it as we want, but neither choice is without huge consequences. Print too little, and the economy literally seizes up, like a car engine running without oil. Print too much, and everything rises in value, people find themselves drunk on inflating asset prices, and the whole balloon eventually bursts.

Governments tried to control the inflationary potential of paper money by pegging it to a high level of gold. The problem here is that this money was often way too hard, especially for debt holding farmers. William Jennings Bryan’s “Cross of Gold” speech was essentially a cry to east coast bankers to soften the value of the dollar and therefore ease the debt burden of Midwestern farmers.

After the Great Depression, capitalist countries tried to steer a middle course with the value of the new global currency- the dollar- pegged to gold under the Bretton Woods system, but with governments following an inflationary policy of high spending even in good times. In the early 1970s this system blew apart: Nixon abandoned the gold peg, and inflation took off like a rocket. This only ended when the central banks, most notably the US Federal Reserve was given real control over the value of the currency, and they took the side of hard-money, only this time it wasn’t based on gold, but on strictly limiting the supply of money itself.

In 1980-81 the chairman of the Federal Reserve, Paul Volcker, essentially convinced the markets that their inflationary expectations regarding the US currency were no longer true, by hanging a sword of Damocles over the American economy’s head. Whenever the American economy grew so fast as to cause inflation the FED would slam on the brakes of money creation and raise interests rates as high as they needed to go to constrict the money supply and squeeze out inflation- even if this lead to rates of unemployment touching 8 percent.

In terms of taming inflation, this certainly worked. In terms of American living standards- not so much. The strong dollar helped push high paying factory jobs overseas. Volcker, and his successor Alan Greenspan effectively ended the rise in American wages by keeping wage inflation, which had previously ran ahead of price inflation being linked to COLAS in labor contracts, under strict control.

Greider’s work leaves us off in the 1990s, but it is easy to pick up the story from there.

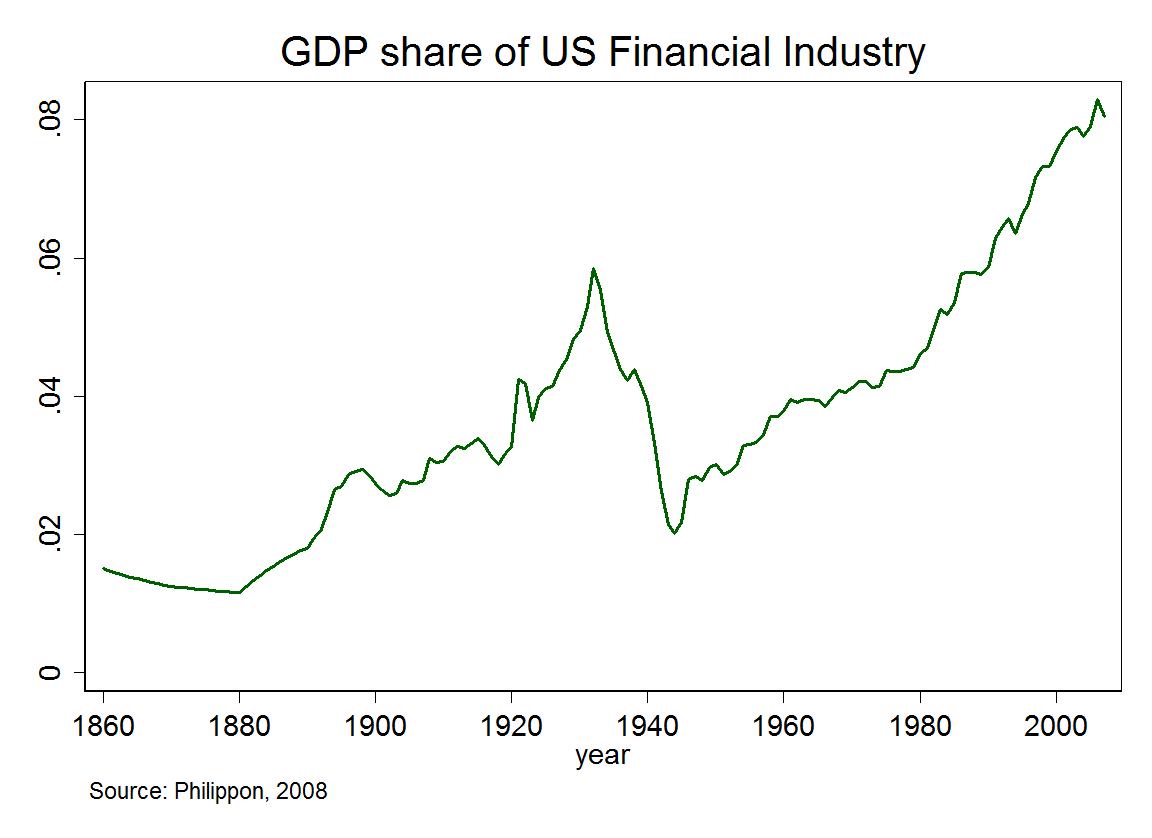

During the same time American wages stagnated, the financial innovations and speculation that were discussed in my post on the quants proceeded apace. The “net-worth” of the middle class became tied not to income, which was frozen in time, but to assets- the value of their homes, and their stock-portfolios, both of which seemed to expand towards the stars. Eventually the staid deposit-banks themselves wanted in on the action- the road to systemic collapse. For many, including the quants, the best way to make money, it seemed, was to have “money beget money”, in the Medieval phrasing, or, to use our modern flavorless terminology- “financialization.”

The graph below captures the transformation:

We know where that led.

Whether or not it needed to be done to save the economy, it makes perfect sense that the FED, which had spent a generation fighting for hard-money despite its costs on the working class and poor, would totally reverse course and move towards soft money; it was saving itself. Opponents of the FED on the right have it only half correct- the problem with the FED isn’t that it aims at weakening the currency, the problem, it seems, is that the FED will only definitively do this when the interests of its primary constituency- the financial sector itself- is at stake, and not, it seems, for any broader public interest.

All this, by the most circuitous route imaginable leads me back to the spell-casters with whom I began this post. These were working class kids, and they really were just kids, even if they were living independently, who were living near Bethlehem, Pennsylvania- a place that a generation before had possessed one of the most vibrant steel industries in the world. By the early 1990s the industry and its hard- but- certain road to the middle class was gone. These kids had no hope of college and made their living working in warehouses moving around goods made overseas, or in malls selling the same, both bought with strong American dollars.

How surprising is it then, that with a hard- but- certain road closed, they would turn to a seemingly easy, yet probabilistic one? The worldview of the spell-casters seems to resemble the fantasies and nightmares of the quants, in the same way Graeber writes of tribal peoples who projected the world of their Western conquerors into strange nightmares of warlocks and zombies. The spell-casters had their Aleister Crowley, and the quants had their Alpha. Both were trying to load the dice in their favor, for to not win the game was to look out onto a future of bleakness.

Another interesting piece. What do you know/are your thoughts on mutual credit? Specifically as it relates to investment? I am not opposed to the idea per se, I just don’t think there are the same incentives to save, or liquidity to invest as there is with an interest-loan system, but I really don’t know all that much about it.

Hank,

In terms of mutual credit, I’d have to say I don’t know much of anything. The whole, Bitcon thing seems interesting to me- in so far as it seemed to be a way to sever the relationship of money to the state, and I think we should realize that there are whole alternatives to the interest-based system we have e.g. Islamic Finance. The problem with these non- interest systems, from my view, is not so much that they reduce the incentive to save or invest, as they reduce the incentive to lend. Muslim countries are credit-poor in the sense that a regular person can’t get a loan to say buy a house or send his kids to college. I am not sure how we can preserve the credit availability of our current system, and at the same time move away from interest, or the far-too-close relationship of finance with the state- but both are things I think we should be thinking about.

By the way, I ended up checking out the Anthony Migchles site. I decided to follow it because I think it is something I should keep an eye on. While his ideas regarding alternative currency systems, and the relationship of our such systems with the state, both now and in the past, are ones I think important to explore, the way he goes about I find HIGHLY DANGEROUS: I mean Ron Paul a Satanists?- come on man! There’s the whole- Freemasons, Jews, Illuminati paranoia that ended up in gas chambers within the lifetime of people still walking around. To draw philosophic connections is one thing, to suggest that what got us to the point was some kind of cabal of the forces of evil is quite another.

After all, it’s not like we don’t have quite reasonable descriptions of what is going on:

http://www.theatlantic.com/magazine/archive/2009/05/the-quiet-coup/307364/

without having to resurrect the damned Protocols of the Elders of Zion.

Sorry for the long-winded answer.

On a totally different note: I heard this story on the radio the other day:

http://www.npr.org/player/v2/mediaPlayer.html?action=1&t=1&islist=false&id=159373770&m=159931382

and thought “I wonder what Hank’s take on that would be”.

Would you mind sharing your thoughts?

Lastly, no word yet from G, might still be in Greece.

I cherish every word of your reply. I didn’t even think of the fact that loaning itself would be down. I mean who would lend a single thin dime that not only are they out for a prolonged period of time, but there is no additional incentive. Anyways, the conspiracy hysteria surely doesn’t help their cause. I will check out the clip. Not sure what it is yet, but knowing you it should be worth the listen and maybe even a ponder or two. Also, good to get an update on Giulio.

My view of it is this: Part of the reason you would lend out money in a non-interest system is for precisely the same reason that you would do it today- that is, if the person asking for the loan had found themselves in need and was your brother, friend, or cousin.

The other reason I think people lend out money in non-interest systems looks a hell of a lot like the same reason people make political contributions today (outside of the belief that the candidate they are supporting was the person they thought was best for the country), and that is to secure a relationship in the hope of wielding future influence. Someone with a pile of capital might lend a merchant a significant chunk of change because this merchant had great political or business connections, or he was hoping to establish connections because he thought the merchant’s endeavor had a good chance of success.

The problem with these non-interests systems is that the people most desperate for a loan are usually the people whose families are generally poor (so they have no one to turn to for a loan),

or lack important connections. For the vast majority of human history these debtors have been farmers who have been driven into debt by the vagaries of harvests or the failure to specialize (say to grow grapes) at the right time.

Here you get usury, which is not just interest rates, but punishingly high interest rates. Usury leads to horrors such as parents putting up children for collateral, and the shear human cost of it was why all major world religions banned the practice.

Getting away from an interest-based system, or better the type of society we have which is based on massive public and private debt, would seem to me to be a good idea, but I have no idea how we would do this given the fact that compelling finance to offer loans at little or no interest would, over the long-haul, probably result in the kinds of loan scarcity we see elsewhere.

The FED and other central banks are actually keeping interest rates at rock-bottom level right now, but the reason is that our society is so in the hole that people are having a great deal of difficulty taking on more debt, and thus the economy continues to grow at a snail’s pace.

Someone might propose that we raise wages so that working and middle class people can afford to pay for common purchases such as cars, homes etc without having to take out debt, but it seems to me this would pretty quickly be lost in price increases.

One could, like Dave Ramsey, try to make this a person, moral issue and convince people not to go into debt, but my feeling is that if everyone heeded his common sense advice, the whole economy would collapse because the entire employment/production structure is predicated on over consumption, so much so, that people better off almost never buy the house or car they can afford in cash, but the one just above that level.

How to escape this dilemma, I haven’t a clue.

I wonder if the effects of the Fed’s low interest rates, particularly bubbles, would be found in a primarily zero-interest system. Or if the amount of money being lent that actually had an effect on the economy would be so small as to skip the bubble phase and go straight to a depression.

I think it is in most individual’s best interest to stay debt free, even if they have to forgo or put off things like college, home ownership, or easy transportation. But at the same, time, if everyone was to do this, you would have a lot less college graduates, home owners, and people driving to work, which may or may not be a net drag on the economy.

I begin to see the dilemma.

A great post!

I want to comment more but I want to finish the Graeber book first so it might be a few days.

Also, I don’t know if you ever read my post Eros, Thanatos, and Tantra but I talk in it about the book Life Against Death by Norman O. Brown. Although my post is completely unrelated to this topic, there is an interesting chapter in the book called “Filthy Lucre” which discusses the psychoanalytic meaning of money. The book, by the way, is utopian in that it attempts to understand history from a psychoanalytic view – basically a history of disease from which we will eventually cure ourselves. In Brown’s view, money is part of our illness.

Thanks, James.

No I hadn’t read your Eros, Thantos, Tantra post, but I wish I had- it was fantastic! An excellent synthesis of pycho-analysis, evolution, and eastern mysticism.

I encourage people to check it out:

It may seem utopian to imagine a society without money, and I personally can’t do so, but in the long-view, something I think you consistently aim for with your blog, maybe not so much. After all,

we’ve been around, what?, a million years, and only had money, in any way that we understand it, for a few thousand of those.

If we really do manage to make it even 10,000 years out, should we really think we’ll still be obsessed with this strange human invention that so dominates our lives? My guess is not, but who knows what comes after, or when.

I also wanted to apologize for Brandon. His modus operandi is a lot of insults and chest thumping, but I want to preserve a diversity of opinion here, so I let him have his say.

Looking forward to your input on my take on Graeber.

Hank,

Interesting question. I couldn’t think of any bubbles in the largest non-interest system out there- the Islamic one- but when I looked it up I found a huge one in the 1980s Souk al-Manakh Stock Bubble in Kuwait.

http://www.stock-market-crash.net/souk-al-manakh/

Like our own recent crisis, it seems to have been the result of a lot of funny money i.e. derivatives being thrown around. The source of the capital in this case was, of course, oil revenues, but without that source of outside money I am not sure how the bubble would have developed in the first place. The place of that outside money is taken up by leverage in our system, and without interests I don’t think you’d likely get these massive loans to financial companies which they use to make the kind of overly massive plays that can sometimes lead to bubbles.

Another thing that I think might be important is the differential interests rates between countries.

Japan has had an almost zero rate of interest for well over a decade, and, from what I understand this led to an enormous carry trade i.e. people borrowing money for close to nothing in Japan and then investing it in Western bonds and stocks “certain” to bring a greater return than zero.

Any movement to a non-interest system would almost have to require capital controls- otherwise the money would be sucked right out of the country.

Thanks.

Rick,

I think you are definitely right about the money having a sort of magical property,

Graeber’s book when I first starting reading it struck me as a very original view on money and debt, but when I look at Brown’s Life Against Death written in 1959 I find many of the same ideas. I am not sure of all of Brown’s sources but some of these ideas have been out there for a while. Let me toss out a few quotes from that book:

After quoting the famous Adam Smith arrow maker text, Brown writes “… it is a safe generalization to say that the postulates of classical economic theory have no relation whatever to the anthropological facts. Archaic economics is not governed by the psychology of economizing calculation… The archaic economy is governed by the rule of giving and sharing.”

Later he writes: “It has been long known that the first markets were sacred markets, the first banks temples, the first to issue money were priests or priest-kings. …If we recognize the essentially sacred character of archaic money, we shall be in a position to recognize the essentially sacred character of certain specific features of modern money – certainly the gold standard, and almost certainly also the rate of interest… Measured by rational utility and real human needs, there absolutely no difference between the gold and silver of modern economy and the shells or dogs’ teeth of archaic economy.”

These observations, however, are not even Brown’s main point. They are more building blocks to the idea that finds money originating in the magical thinking and infantile eroticism of the child – the same source from which arises the religious guilt industry. Ultimately growing up would free us from both the guilt complex and the money complex.

I must admit that Brown is not the accessible of sources and reading him can be a difficult since his breadth is great and understanding requires quite a bit of familiarity with Freud and psychoanalytic terms. Graeber is a much easier read.

I think perhaps with money and debt we see literally how culture works – specifically how the human psychic organization creates cultural artifacts and imbues them with existence, where in fact them have none, to serve the goal of social organization and preservation of a power structure.

James,

I think these anthropological and historical findings regarding the nature and history of archaic money being found in Brown in 1959 indicate that no one has yet come along to disprove them in all that time, and given how long these ideas have been held, it seems no proof will likely be forthcoming.

Perhaps the role of Graeber has been to bring these ideas to public attention at just the right time,

and in a way that more directly demands neoclassical economists, who have dominated the policy debate for a generation, and helped get us into this mess, justify their underlying assumptions.

Life Against Death sounds fascinating. Perhaps, if I can launch the discussion groups I previously mentioned, we can do something on money and make Brown part of the “required reading” or discussion.

[…] alternative to it should be whether old school communist such as Slavoj Žižek or anarchists like David Graeber. Lefties are one thing, the Pope is another, and you’ve got to know a system is in trouble when […]

[…] was especially compelling and thought provoking when it came to that ultimate modern fantasy and talisman that all of us, from Richard Dawkins to, Abu Bakr al-Baghdadi believes in; namely […]

[…] change started quite some time ago with the move away from money backed up with gold to fiat currencies. Those gold bugs who long to […]

[…] communism of the old school such as that of Slavoj Žižek or the anarchism of someone like David Graeber. Leftists are one thing the Pope is another, and you know a system is in trouble when the most […]

[…] other side of the political spectrum, are anarchists who think the problem is power and therefore purging THE MACHINE of power relations, and decentralizing its functions, would leave us with human- made world that would re-emphasize […]